It is no longer news that every bottle of water, every can of drink and every glass of wine carries a price tag shaped by forces most consumers never see. Today, these forces include the cost of oil, the price of aluminum, the availability of plastic, the length of a shipping route, among others. Since late February 2026, all of those forces have been upended at once. The closure of the Strait of Hormuz, one of the most critical waterways in the world, is sending shockwaves through the global beverage industry. And in this week’s Drinkabl’s deep dive, we explore how.

On February 28, 2026, the United States and Israel initiated coordinated airstrikes on Iran under Operation Epic Fury, targeting military facilities, nuclear sites, and key leadership. Within hours, Iran’s Islamic Revolutionary Guard Corps issued warnings prohibiting all vessel passage through the Strait of Hormuz, triggering an effective halt in shipping traffic through the narrow waterway that connects the Persian Gulf to the rest of the world’s oceans.

Industry watchers and analysts have described it as the biggest energy crisis since the oil embargo of the 1970s, and notably, Iran did not need a naval blockade to bring traffic to a halt. A handful of drone strikes in the vicinity of the strait was enough to convince insurers and shipping companies that the route was too dangerous to traverse.

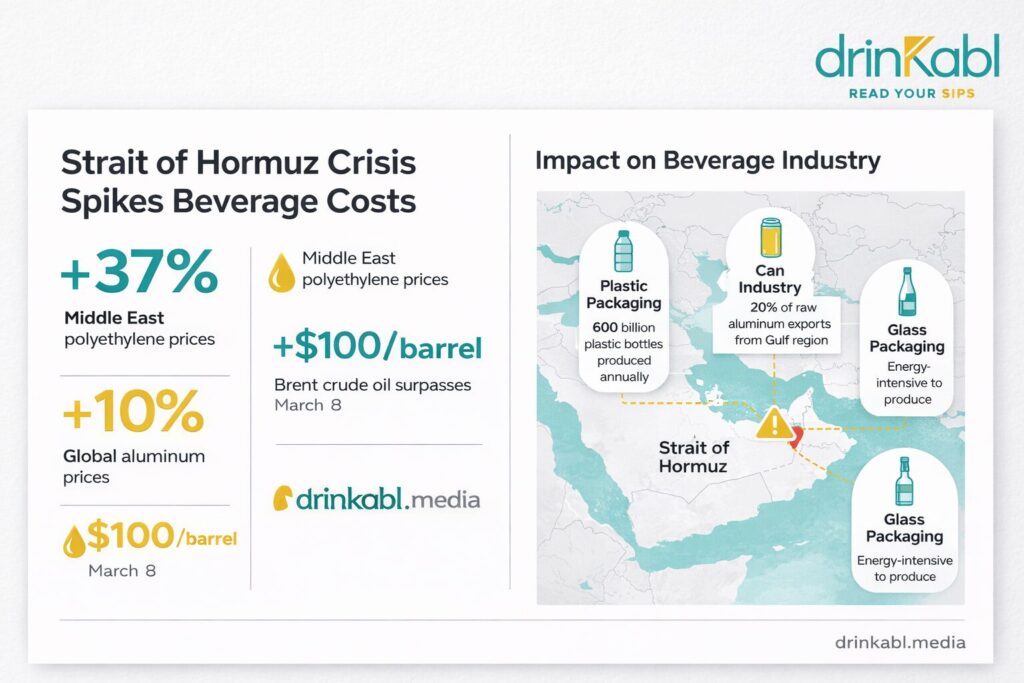

The energy shock has been immediate and severe. Brent crude oil prices surpassed $100 per barrel on March 8 for the first time in four years, rising to $126 per barrel at their peak. But for the beverage industry, the crisis extends far beyond the fuel pump.

The most direct blow has landed on packaging. An estimated 40 percent of global plastic packaging is dedicated to the food and beverage sector, and roughly 600 billion plastic bottles are produced globally for water alone every year. That packaging depends heavily on petrochemical inputs and the vast majority of Middle East polyethylene capacity, used in bottles and packaging, as well as regional exports of methanol, ethylene glycol and polypropylene, all depend on the Strait of Hormuz for export. Polyethylene and polypropylene prices saw their largest monthly increase in 25 years over the 30 days following the closure. In Asia, the situation has been particularly acute, with commodity analysts noting that many companies have already declared “force majeure,” a legal mechanism to pause supply obligations because they lack enough fuel to run their petrochemical facilities.

Aluminum, the material that keeps billions of canned beverages cold and shelf-stable, is under similar strain. Gulf states account for around 20 percent of raw aluminum exports and 8 percent of global aluminum production, and aluminum prices have risen since the closure began. The UAE and Bahrain are among the top six aluminum-producing countries in the world, and packaging is particularly vulnerable to volatility in aluminum markets. Aluminum prices have already risen 10 percent, and some of the sectors most affected by these disruptions are food and beverage manufacturers.

Glass, which is still the packaging of choice for beer, wine, and spirits, faces its own crisis. Glass is a notoriously energy-intensive material to produce, and price impacts have already been observed, with knock-on effects expected for makers of beer, wine, and spirits.

Then there are the beverages themselves. Tea is currently the commodity most directly impacted by the closure. The UAE, Iraq, Iran, and Saudi Arabia are among the world’s largest importers of tea, and with shipping through the strait disrupted, the supply chain for one of the world’s most consumed beverages is under serious pressure. Coffee, another global staple, faces compounding risks: while prices had been declining thanks to bumper crops in Brazil and Vietnam, higher fuel costs and longer shipping routes are now threatening to push them back up. Sugar, a core ingredient in soft drinks, juices, and energy drinks, is also exposed to the disruption, as the conflict drives up the cost of transporting goods between producing and consuming nations.

For beverage producers, the problem is not just what is happening today but what comes next. “For beverage producers, the issue is less about availability today and more about reliability tomorrow,” one industry analyst noted, adding that disruptions around critical shipping routes are increasing transit times and freight costs, already feeding through into higher fuel and insurance pricing.

The rerouting of ships around Africa’s Cape of Good Hope, now the only safe alternative to the closed strait, is adding weeks to delivery times and cost. Major container shipping companies including Maersk, CMA CGM, and Hapag-Lloyd suspended transits through the strait and related routes, while Houthi-controlled Yemen simultaneously announced it would resume attacks on commercial ships in the Red Sea, forcing Suez Canal traffic to also be rerouted around Africa. That double blow has effectively shut both of the world’s most important maritime shortcuts simultaneously.

Beyond the immediate disruption to trade, the effective shutdown of the waterway has raised longer-term questions about how shippers will conduct their business in the future. “I think, given the geopolitical uncertainties we’re currently seeing, this is likely going to be a permanent feature of risk management rather than just a temporary response to the Iran war,” Nick Marro, the Economist Intelligence Unit’s lead analyst for global trade, said on Al Jazeera.

For consumers across the world, whether in London, Lagos, or Lahore, the message from industry observers and analysts is straightforward: the price of a drink is going up, and it may stay up. Experts predict the impact on consumer goods will be felt for 12 to 24 months, even if the geopolitical conflict is resolved quickly. The world’s beverage industry, built on tight margins and predictable supply chains, now faces a period of deep uncertainty, with no clear timeline for when the waters of the Strait of Hormuz will flow freely again.

Jack Daniel’s X Jameson: A Look At The Merger That Could Potentially Humble Johnny Walker

There is always a time in every industry when the second and third largest players look at each other across the table, look at the leader sitting comfortably above them, and decide that the only rational move is to stop competing with one another and start competing together. The global spirits industry may have just reached that moment.

The confirmation last week that Pernod Ricard and Brown-Forman are in early merger discussions sent shockwaves through the drinks trade, and for good reason. If this deal happens, it would unite some of the most recognisable bottles on the planet: Jameson Irish whiskey, Absolut vodka, Beefeater gin, Jack Daniel’s Tennessee whiskey, Woodford Reserve bourbon, and Herradura tequila, all under one roof. It would be, by almost any measure, a big moment for an industry badly in need of one.

Indeed, the premium spirits boom that followed the pandemic, the golden window when consumers worldwide were splashing out on top-shelf bottles and the industry could do little wrong, is over. Tariffs and supply chain woes have made the category even more difficult, and all three of the major players have seen sales and share prices fall. Brown-Forman endured eight consecutive quarters of year-over-year sales declines before recently posting its first positive growth numbers. Pernod Ricard’s shares fell to levels not seen since 2009 before the merger news briefly lifted them. Even the mighty Diageo, which sits at the top of this market with Johnnie Walker, Guinness, Smirnoff, Baileys, and Captain Morgan in its portfolio, saw its U.S. sales fall 7% in its first half.

Indeed, this is not accidental as consumers have grown more selective. Health-conscious younger drinkers are moving away from alcohol altogether. The sober-curious movement is no longer niche. Inflation has squeezed discretionary spending. And in the United States, tariff uncertainty has added a layer of unpredictability that no brand manager can plan around with confidence. Major spirits companies are sitting on a $22 billion glut of unsold aged inventory, the largest in a decade, a stark sign of how dramatically the market has shifted.

Against this backdrop, the logic of a Pernod Ricard and Brown-Forman combination is arguably overdue. A merger could create a global spirits entity with a market cap of around $30 billion and volume of nearly 200 million nine-litre cases, ranking second to Diageo in the category. Analysts at Jefferies estimate a merged company could save up to $450 million annually by combining Brown-Forman’s whiskey and tequila brands with Pernod’s global distribution network.

What makes this potential union particularly interesting is that the two portfolios are genuinely complementary rather than redundant. Brown-Forman’s great strength is American whiskey and the U.S. domestic market. Pernod Ricard’s great strength is its sprawling global reach and a balanced portfolio that spans Scotch, Irish whiskey, gin, vodka, champagne, and cognac. Brown-Forman would provide Pernod Ricard with a much more solid foothold in the United States, where the French group has long lacked the scale to properly compete with Diageo. And Pernod’s distribution machinery would give Jack Daniel’s and Woodford Reserve a more powerful global launchpad than Brown-Forman has been able to build independently.

For the African market and Nigeria in particular, a combined entity would matter enormously. Diageo’s dominance in this region, and a formidable local manufacturing presence, has long gone largely unchallenged by international spirits rivals. A larger, better-resourced Pernod-Forman combination would have both the portfolio depth and the financial firepower to invest more aggressively in emerging markets where the demographics point stubbornly upward.

But we should not pretend this is a straightforward deal. No partnership is without its challenges. The Brown family controls over 67.5 percent of Brown-Forman’s voting shares and has historically resisted takeovers. The Ricard family, meanwhile, retains 21 percent of voting rights in Pernod Ricard. Any deal would require both founding families to agree not just on price, but on governance, leadership, headquarters, and the delicate question of whose culture and identity shapes the combined company. These are rarely easy conversations, and history is littered with mergers-of-equals that quickly became something far messier.

There is also the question that no amount of synergies can fully answer: where does growth come from? Analysts have noted bluntly that a merger alone does not solve the sector’s main problem, which is boosting sales growth. Cutting costs and combining distribution networks improves profitability but does not, by itself, make consumers drink more premium whiskey. The industry’s underlying demand challenge requires innovation, brand investment, and a credible answer to the question of what spirits offer the next generation of drinkers. A merger could also reduce the number of buyers and distributors available to independent brands, a consequence the wider industry will watch closely.

Still, the direction of travel seems clear. The spirits industry is consolidating, and those who move first and boldest will shape what the competitive landscape looks like a decade from now. Diageo has held the top position in this market for a long time, in part because no single rival has had both the scale and the portfolio to mount a sustained challenge across all categories and all geographies simultaneously. A merged Pernod Ricard and Brown-Forman would, for the first time, come close.

Diageo should be watching very carefully. The king of spirits may finally have competition worthy of the name.

Read More:

- The Thirst Crisis That Could Break the Beverage Industry

- Is Your Smoothie Actually Healthier Cooked? New Science Rewrites the Rules on Pasteurisation

- Who Is Silencing South Africa’s Sugar Warning? Inside the ARB’s Conflict of Interest Crisis

- Nigeria’s Bitters Category and the Rise of Citrus-Infused Herbal Drinks