A record-breaking quarter and a sweeping C-suite overhaul signal that Monster Beverage is done treating global markets as an afterthought.

Monster Beverage Corporation didn’t just report its strongest quarter in company history last week, it simultaneously tore up its organizational chart.

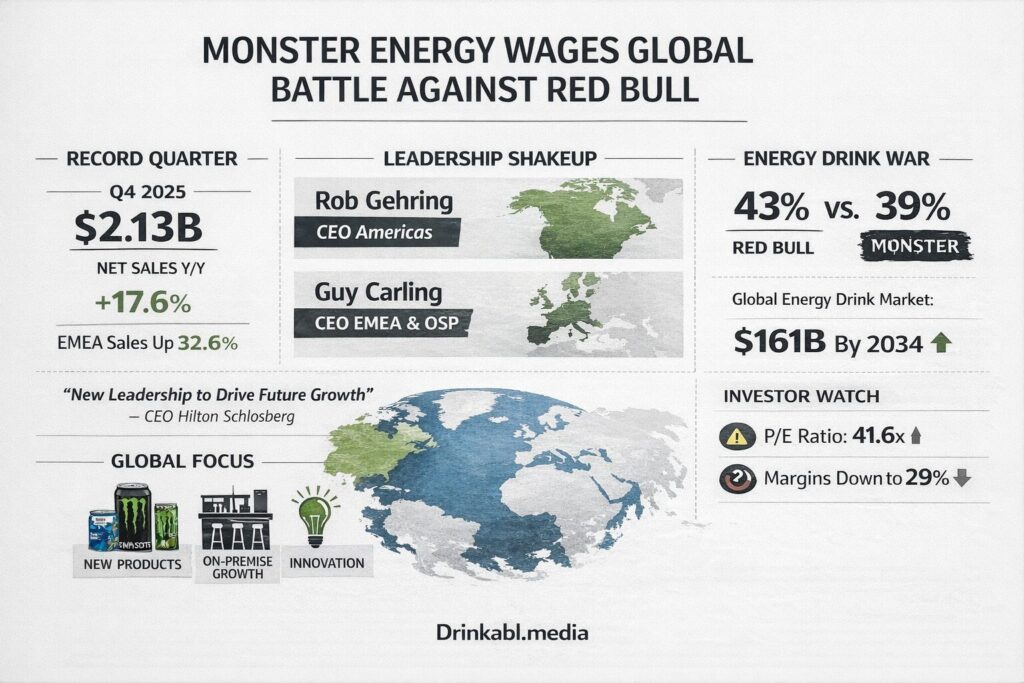

On February 25, 2026, the Corona, California-based energy drink giant announced a series of leadership appointments that took immediate effect, elevating Rob Gehring to CEO of the Americas and naming Guy Carling, a Monster veteran of nearly two decades, as CEO of EMEA & OSP. Emelie Tirre, previously Chief Commercial Officer, steps into a newly created Chief Strategy Officer role, overseeing enterprise-wide planning.

The timing was anything but coincidental.

Monster’s Q4 2025 net sales crossed the $2 billion threshold for the first time in company history, rising 17.6% to $2.13 billion. Sales outside the United States surged 26.9%, climbing to roughly 42% of total net sales — up from 39% a year earlier. EMEA alone posted a staggering 32.6% increase in dollar terms.

CEO Hilton Schlosberg was unambiguous about the intent behind the restructuring.

“We believe the leadership changes that we are announcing today will drive future performance and growth across the business.”

The move is widely read as an acknowledgment that Monster’s international business has outgrown a centralised management model. Elevating Gehring and Carling into dedicated regional CEO roles aligns decision-making with where a large share of growth is now coming from, while moving Tirre into a pure strategy role centralises long-term planning across pricing, product mix, and expansion priorities.

The structural shift comes at a pivotal moment in the global energy drink wars. Red Bull currently holds approximately 43% of the global energy drink market, while Monster commands around 39%, a gap the new leadership architecture seems designed to narrow. The global energy drinks market, valued at roughly $84 billion in 2025, is projected to reach $161 billion by 2034, making regional execution not just a competitive advantage but an existential necessity.

Monster is also playing an aggressive product game to feed that international appetite. Innovation remains central to the company’s long-term growth strategy, with new product offerings planned throughout 2026 , from Juice Monster Voodoo Grape to a zero-sugar Lando Norris Formula 1 edition, all targeting younger, globally-minded consumers.

Strategic focus for 2026 also includes expanding Monster’s Foodservice and On-Premise business to capture growth in non-tracked channels. For a brand that has built its empire through convenience stores and petrol forecourts, cracking on-premise, bars, restaurants, venues, would represent a meaningful new frontier. It’s a space Drinkabl knows intimately, where the battle for shelf space and pour lists is just as fierce as the supermarket aisle.

Investors, however, are watching the numbers as closely as the org chart. At $81.06 per share (NasdaqGS: MNST), Monster’s stock trades at a P/E of roughly 41.6 against a beverages industry average closer to 25.7, a premium that demands the new leadership team deliver. Adjusted operating expenses surged 21.4% year-over-year in Q4, outpacing revenue growth and compressing operating margin to 29% from 32.1% in the prior quarter. Aluminium cost headwinds and a complex tariff environment add further pressure.

How quickly the new Americas and EMEA leaders translate recent sales momentum into sustained performance, and whether international growth supports or compresses margins, will be the defining question of 2026.

For now, the message from Monster is clear: the beast is no longer American. It’s global, and it’s just hired the team to prove it.

Further Reading on Drinkabl:

Hypo Bleach Not A Drink, Brand Handlers Issue Warnings

NESCAFÉ Moves Into Ibadan’s Busiest Bus Park

‘Kill Me Quick’ Factory Busted, Hidden Between Two Churches

Nigerian Beverage Plants Are Haemorrhaging Money on Energy, And Most Have No Idea Where