For decades, Nigeria’s FMCG growth formula was simple. Go mass. Go affordable. Go everywhere. Sachet packs, deep distribution, and low unit pricing built some of the biggest consumer franchises in the country. It worked. And now, according to Onwudiwe Uche, a brand strategist who has spent years tracking category growth in Nigerian FMCG, the formula is cracking under its own weight.

“Affordability alone is becoming easier to copy, and therefore weaker as a long-term competitive advantage,” Uche wrote this week in an assessment that cuts through a lot of the noise about Nigeria’s consumer market. “That is the real disruption.”

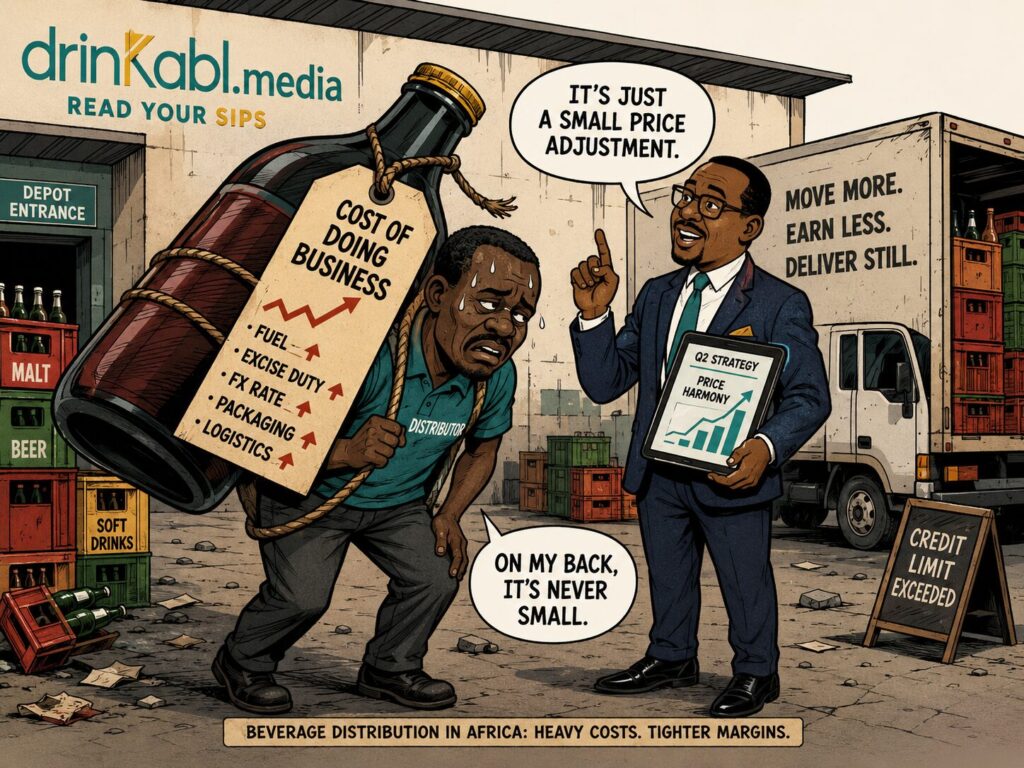

The macroeconomic backdrop makes his argument hard to dismiss. Nigeria’s GDP is projected to grow at 4.4% in 2026, per both the IMF and the World Bank, revised upward from earlier estimates in January after improvements in oil production and FX liquidity. But GDP growth and household purchasing power are telling two different stories. Headline inflation, per the National Bureau of Statistics, rose to 15.69% in April 2026, up from 15.38% in March. Food inflation reached 16.06% year-on-year for the same period, driven by staples: garri, beans, yam flour, tomatoes, beef. Every basket is under pressure. Every purchase is questioned. Every brand must now defend its place in the consumer wallet.

The manufacturing picture is equally mixed. The Stanbic IBTC Bank Nigeria PMI registered 52.4 in April 2026, above the 50-point threshold for the third consecutive month. Muyiwa Oni, Head of Equity Research West Africa at Stanbic IBTC Bank, noted that new orders increased in line with higher customer numbers and rising demand, but added that “lingering inflationary pressures limited the pace of expansion” and that “companies increased their selling prices in April to the highest level since December 2024 in response to rising fuel and raw material costs.” The factory may be busier. The profit pool may not be healthier.

That is precisely where the old playbook cracks. Post-2016 recession, sachetisation was one of Nigerian FMCG’s smartest responses to declining purchasing power. A 25ml pack. A smaller portion. A lower price point. It brought categories within reach of consumers who would otherwise have walked away. Uche’s point is not that this was wrong. His point is that it has since become everyone’s answer, and a strategy that every competitor adopts stops being a strategy at all. “Today, it risks becoming a market-wide survival tactic,” he writes. Premium brands are moving down. Legacy brands are defending volume. New entrants are competing aggressively on price. When everyone becomes affordable, affordability itself stops being distinctive.

The real crisis, as Uche frames it, is not the death of the mass market. Nigeria is still a mass market. Affordability still matters enormously. The crisis is the death of undifferentiated affordability as a growth strategy, because price undercutting is no longer a silver bullet. It is increasingly a margin trap. For beverage players specifically, the stakes are high. This publication traced the same fault line in March 2026, reporting how sachetisation in Nigeria’s drinks category was redirecting demand rather than creating it, and how the unregulated low-price segment was quietly absorbing the consumers that formal brands were trying to hold.

What makes Uche’s analysis sharp is that it reframes the question from cost to value.

“Consumers are no longer simply asking: ‘Can I afford it?’ They are asking: ‘Is it worth it?’ That changes everything.” That shift does not require a consumer to become wealthier. It requires a brand to become more legible. A shopper choosing between two equally priced sachets of malt drink is already asking a value question. The brand that answers it wins the shelf. The brand that does not will lose the shelf to the next entrant willing to undercut by five naira.

Uche draws three implications for FMCG leadership. Segment the mass market more intelligently, because not all mass consumers are the same and treating them as one block is a strategic mistake that leaves real consumer insight on the table. Move from price accessibility to value justification, which means building the case for why a product is worth buying beyond its price point. And build differentiation beyond advertising, because amplifying an undifferentiated product more cheaply is not a strategy; it is just cheaper noise. “The next growth cycle will not reward brands that simply run faster to the bottom of the price ladder,” he writes.

For Nigeria’s beverage industry, this is not abstract brand theory. It is a description of what is already happening on the shelf: margin compression, volume wars, and a consumer base quietly recalibrating what brand trust means when money is tight. The question Uche ends on is the right one: in the next decade, will Nigeria’s biggest FMCG winners be the brands that are cheapest, or the brands consumers trust most when every purchase has to count?

The Central Bank of Nigeria’s next Monetary Policy Committee sitting will signal how much longer elevated input costs persist, and therefore how much pricing room brands actually have to build value rather than just compete on price. That decision, and what happens to consumer credit in its wake, is the next number FMCG strategists need to watch.

READ MORE: