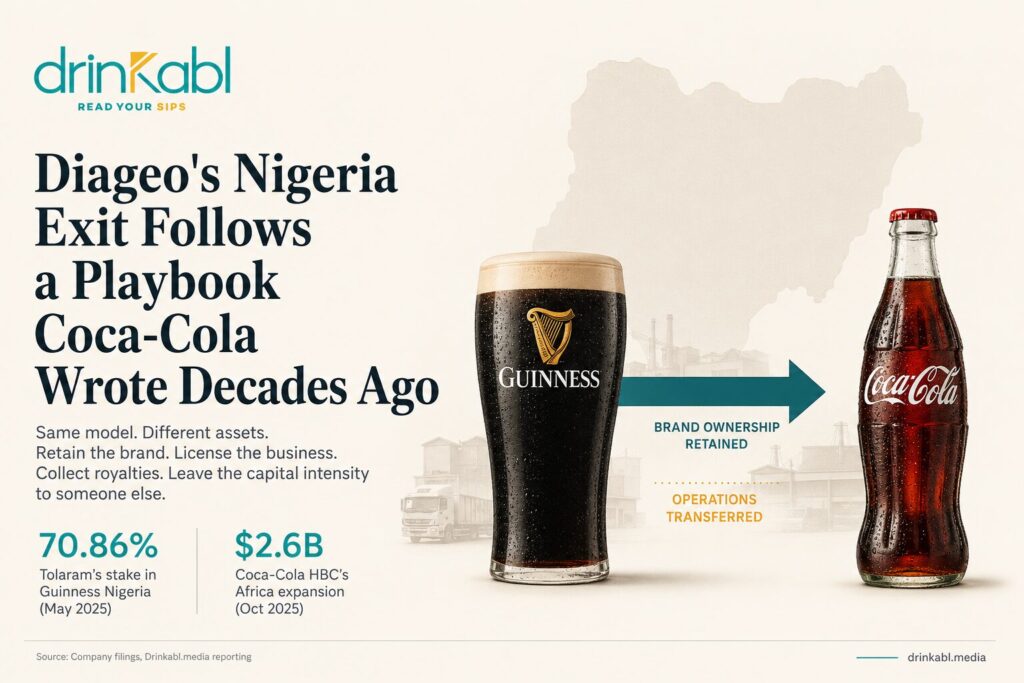

Diageo did not invent the model it used to exit Guinness Nigeria. It borrowed one that The Coca-Cola Company refined across decades and is still actively expanding: retain the brand, license it to a capable local operator, collect royalties, and leave the capital intensity to someone else.

Tolaram’s NGN 103.7 billion acquisition of Diageo’s 58.02 percent stake, completed in September 2024, transferred operational control of a brewery without transferring ownership of a single brand. Diageo kept Guinness. Tolaram got the trucks, the factories, the distributor contracts, and a P&L that had just posted a NGN 54.8 billion loss for the financial year ended June 2024.

The Coca-Cola parallel is not decorative. The Nigerian Bottling Company, which manufactures and distributes Coca-Cola products across Nigeria under Coca-Cola HBC, has operated under exactly this structure for more than 75 years. The Coca-Cola Company owns the brands and drives consumer marketing. NBC handles production, packaging, and last-mile delivery. What Diageo is attempting in beer, Coca-Cola institutionalised in soft drinks before most of Nigeria’s current brewers existed.

The financial logic is the same on both sides. Coca-Cola’s global refranchising strategy has reduced bottling investment from 52 percent of total revenue in 2015 to 13 percent by 2024, redirecting capital toward concentrate production and brand management. Diageo’s Nigerian exit follows identical arithmetic: royalty income without operational exposure, brand equity without balance sheet risk.

Where the models diverge is in what each incoming operator brought. Coca-Cola HBC built its Nigerian operation from the ground up over seven decades, compounding distribution infrastructure, retailer relationships, and cold chain presence across that entire period. Tolaram arrived in the beer business in 2024 carrying four decades of consumer goods experience, Indomie-built route-to-market reach, and logistics infrastructure from the Lagos Free Zone. It is a credible substitute. It is not the same thing.

The early numbers favour Tolaram’s bet. Guinness Nigeria returned to profitability under new ownership, posting NGN 16.2 billion in net earnings for FY2025, with revenue growing 144 percent over the 18-month period ending December 2025. Q1 2026 pre-tax profit reached NGN 15.7 billion, up 53 percent year-on-year. The company paid its first dividend in two years in March 2026, at NGN 2.00 per share. Drinkabl.media’s coverage of the Q1 results attributed the recovery to structural cost reduction and distribution efficiency. CEO Girish Sharma confirmed in late 2025 that the company had expanded into northern states previously underleveraged under Diageo’s structure, with Malta Guinness carrying most of the commercial weight in those markets.

Coca-Cola HBC’s parallel commitment to Africa has moved in the opposite direction: deeper, not lighter. In October 2025, the Swiss-based bottler announced a $2.6 billion acquisition of a 75 percent stake in Coca-Cola Beverages Africa, adding 14 new markets including Kenya, Ethiopia, and South Africa. The deal, pending regulatory clearance expected by end-2026, would give Coca-Cola HBC control of roughly two-thirds of Coca-Cola’s total African volume and coverage of more than half the continent’s population. That is not the posture of a system retreating from local operational exposure. It is the posture of a system that has decided trusted local operators running at scale are the durable structure.

Drinkabl.media’s reporting on Diageo’s concurrent exit from East Africa shows the same asset-light instinct playing out in a different context, with Asahi acquiring the EABL operation Diageo is vacating. Nigeria and East Africa are different experiments running simultaneously: one tests whether a non-beverage conglomerate can operate an inherited brewery, the other tests whether a foreign brewer can build local depth quickly enough to justify the acquisition price.

The Financier Worldwide analysis of the CCBA deal notes that bottling investment as a share of Coca-Cola’s revenues is projected to fall to approximately five percent after the transaction closes. Diageo’s royalty model in Nigeria points toward the same destination from the other direction.

Tolaram’s mandatory takeover offer, finalised in May 2025, raised its Guinness Nigeria holding to 70.86 percent. The governance structure is clear. The dividend is flowing. Distribution is expanding. What remains unresolved is whether the licensing structure holds its commercial logic if Nigeria’s beer volumes, which declined by mid-teens across 2025, do not recover. That is the question the proposed 2026-2028 excise duty framework will force into focus faster than either party probably anticipated. Coca-Cola HBC and The Coca-Cola Company had 75 years to calibrate what each side owes the other when the market turns difficult. Diageo and Tolaram are still in year two.

READ MORE