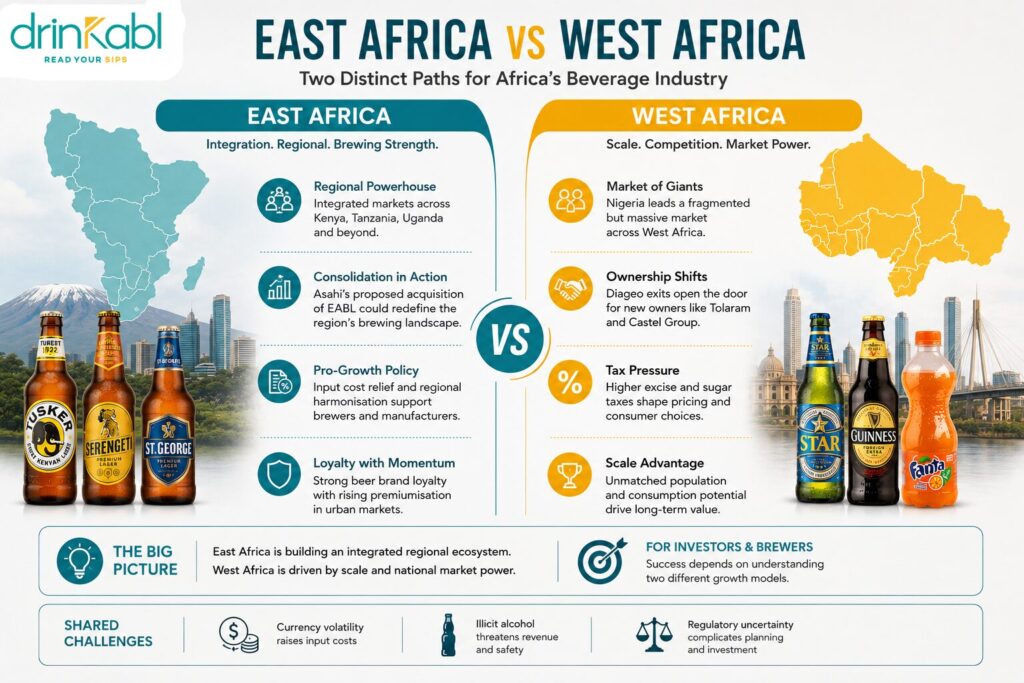

Africa’s beverage sector is undergoing one of its biggest transformations in decades, driven by ownership changes, tax reforms, shifting consumer behaviour, and growing indigenous competition. While East and West Africa face many of the same pressures, they are evolving along distinctly different paths.

At the heart of the divergence is market structure. East Africa increasingly functions as a regional beverage ecosystem anchored by cross-border operators and regulatory coordination, while West Africa remains dominated by large national markets, particularly Nigeria.

| Dimension | East Africa | West Africa |

| Market Model | Regional integration | National-scale competition |

| Dominant Structure | Regional champion-led | Country champions |

| Key Markets | Kenya, Tanzania, Uganda, Ethiopia | Nigeria, Ghana, Côte d’Ivoire |

| Ownership Trend | Consolidation around EABL/Asahi | Fragmented ownership transitions |

| Regulatory Approach | Regional harmonisation through EAC | Country-by-country regulation |

| Tax Direction | Input-cost relief for producers | Higher consumer-facing excise taxes |

| Consumer Culture | Beer and malt-led loyalty | Beer plus growing soft-drink taxation focus |

| Indigenous Challengers | MeTL, Bakhresa | Tolaram, emerging premium local brands |

| Key Strategic Story | Asahi-EABL acquisition | Diageo exits and tax reforms |

| Long-Term Advantage | Regional scale and integration | Population and market size |

The defining corporate story across both regions is the gradual dismantling of Diageo’s historic African beer empire.

In East Africa, Asahi is pursuing the acquisition of East African Breweries Limited (EABL), potentially gaining control of one of the continent’s most powerful brewing platforms spanning Kenya, Uganda and Tanzania. If approved, the deal would represent one of the largest foreign investments in African consumer goods in recent years and could reshape competitive dynamics across the region.

In West Africa, Diageo has already completed a series of exits. Guinness Nigeria has moved into the hands of Tolaram, while Guinness Ghana has been acquired by Castel Group. Earlier, Diageo sold Ethiopia’s Meta Abo Brewery to Castel. The result is a significant redistribution of beer assets across Africa.

The broader pattern suggests multinational beverage companies increasingly view beer as a local operating business requiring extensive manufacturing and distribution infrastructure, while retaining greater interest in higher-margin spirits portfolios.

The buyers tell their own story. Asahi represents global brewing capital seeking growth in Africa’s expanding beer markets. Tolaram represents something different: the rise of distribution-led investment. Having built one of Nigeria’s strongest consumer-goods networks through Indomie noodles, Tolaram is betting that retail reach can be as valuable as brewing expertise.

Policy trends reveal another major divide.

East African governments, particularly Kenya, are increasingly using fiscal policy to support domestic manufacturing. Proposed reductions in excise duties on industrial alcohol inputs would lower production costs for beverage companies and potentially improve margins for producers.

West Africa, especially Nigeria, is moving in the opposite direction. Policymakers are pursuing stronger taxation of sugar-sweetened beverages and maintaining pressure through alcohol excise frameworks. These reforms are being driven by a combination of revenue needs, public-health objectives, and broader fiscal-reform programmes supported by international institutions.

The result is a striking contrast: East Africa is experimenting with measures that lower production costs, while West Africa is increasingly focused on taxing consumption.

Consumer behaviour also reflects important differences.

East Africa remains strongly associated with national flagship beer brands such as Tusker, Serengeti and St. George. Brand loyalty remains a defining characteristic of the region’s beer culture, although premiumisation is gaining momentum among urban consumers.

West Africa shares similar loyalty dynamics but often with greater market concentration. Côte d’Ivoire’s Solibra remains a dominant force, while Nigeria’s beer market continues to be shaped by intense competition among Nigerian Breweries, International Breweries and Guinness Nigeria.

Soft drinks represent another emerging battleground. Tanzania stands out as one of the few African markets where Pepsi has historically challenged Coca-Cola’s dominance, aided by local competitors such as Azam Cola. Nigeria, by contrast, remains overwhelmingly Coca-Cola territory, with no indigenous cola challenger operating at a comparable scale.

Both regions face common challenges. Currency volatility continues to increase the cost of imported inputs, while illicit alcohol remains a persistent threat whenever excise taxes rise. Regulatory uncertainty surrounding mergers, acquisitions and tax policy also complicates long-term planning.

However, the risks differ in intensity. East Africa’s biggest uncertainty centres on the outcome of the Asahi-EABL transaction and the future direction of regional integration. West Africa’s greatest challenge remains policy unpredictability, particularly in Nigeria, where beverage taxation frameworks have undergone repeated revisions in recent years.

Ultimately, neither region is following a superior model. Instead, they represent two distinct versions of African beverage-market development.

East Africa is emerging as the continent’s most integrated beverage region, supported by regional institutions and cross-border operators. West Africa, led by Nigeria’s enormous consumer base, remains Africa’s most commercially significant beverage market.

For investors, brewers and consumer-goods companies, understanding the difference between integration-driven growth and scale-driven growth may prove more important than any individual transaction or tax reform currently making headlines.

READ MORE

- Coca-Cola HBC Commits $1.28 Billion to Egypt

- Kenyan Court Clears Way for Asahi’s $2.3 Billion EABL Takeover

- These Are the 20 Nigerian Beverage Companies to Watch in 2026