Two months into the Strait of Hormuz closure, the beverage sector is not stabilising. It is absorbing.

The week of May 4 erased whatever cautious optimism had built around ceasefire talks. The U.S. military fired on Iranian forces in the strait, sinking six small boats; Iran responded by launching missiles and drones at UAE targets, hitting the Fujairah oil hub and striking a tanker near the waterway.

A fragile ceasefire that had held since late March appeared close to collapse. Two American-flagged vessels completed transit under military escort, the first commercial passage in weeks, but no shipping company or insurer has indicated any readiness to resume normal operations. The corridor remains, in every practical sense, closed.

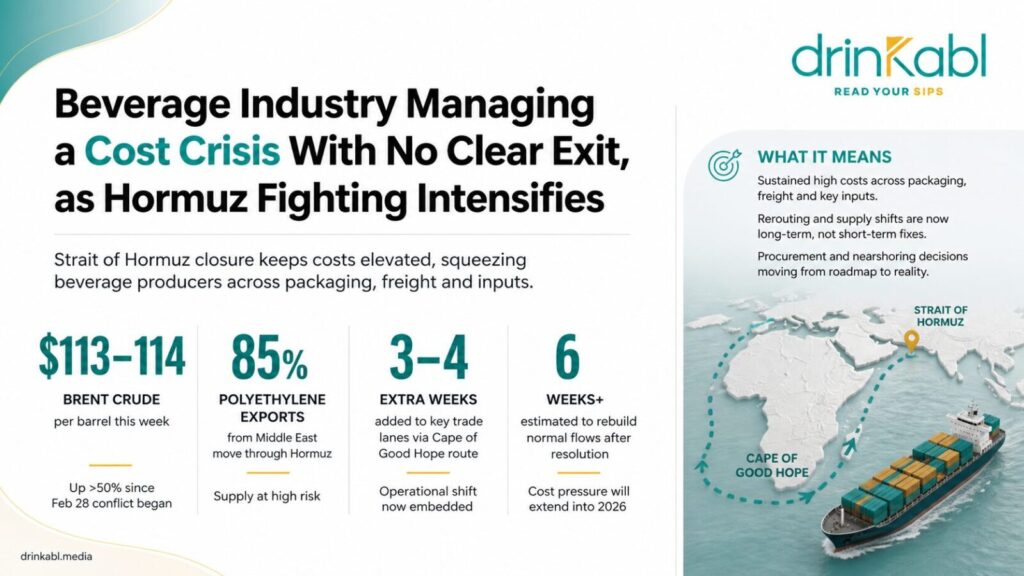

Brent crude is trading around $113 to $114 per barrel this week, up more than 50 percent since the conflict began on February 28. The $126 peak reached in mid-March has not held, but neither has it been forgotten: every escalation sends prices back toward it. Goldman Sachs has flagged accelerating depletion of refined product buffers, particularly petrochemical feedstocks including naphtha and LPG. Supply chain experts warn that equity markets are broadly underestimating the downstream cost impact.

For beverage producers, that is the operating environment for the foreseeable future.

Where exposure has been managed

Companies with diversified procurement and forward purchasing agreements in place before February have absorbed the initial shock better than most. Resin supply contracts locked in during 2025 provided partial cover against the spike in polyethylene and polypropylene prices that followed the closure, significant given that roughly 85 percent of Middle East polyethylene exports move through Hormuz. Early retail data from Europe and North America suggest that where shelf price increases have been implemented, volume has largely held. That resilience may not persist if the cost environment extends deep into the second half of the year.

Aluminium can manufacturers have also moved quickly. Gulf producers are significant aluminium exporters, and the initial price spike was sharp. Manufacturers with established smelter relationships in Europe and North America have rerouted supply at cost, while several have accelerated sourcing from recyclers to increase secondary aluminium in their production mix, a shift that improves resilience well beyond this specific crisis.

Where pressure is acute and worsening

Tea supply chains remain the most directly impaired. The UAE, Iraq, and Saudi Arabia are among the world’s largest tea importers, and all are effectively cut off from normal inbound flows. Producers supplying those markets face elevated freight costs, extended transit via Africa, and buyers who have pulled back on forward orders. Inventory is accumulating at origin or being redirected to secondary markets at discounted terms.

Glass packaging, dominant in beer, wine, and spirits, faces sustained cost pressure with no short-term relief mechanism. Glass production is highly energy-intensive, meaning oil and gas price increases translate almost directly into input costs. Premium producers are absorbing costs that were not in their 2026 operating plans. Several European bottlers have opened discussions with brand partners about lighter bottle specifications. The financial saving is modest; the signal it sends about margin pressure is not.

Coffee illustrates the disconnect between commodity price and operational reality. Green coffee prices had been declining heading into the crisis, supported by strong harvests in Brazil and Vietnam. Global supply has not changed. But freight costs from origin to roaster have risen substantially, and roasters with thin margins and no freight hedging are taking a squeeze the commodity price does not reflect. Consumers will likely face higher shelf prices regardless.

Packaging costs more broadly are the sector’s most acute structural problem. Beyond plastics, the crisis is tightening supply of monoethylene glycol, a key input for packaging and textiles, with significant volumes previously moving through the Gulf corridor. Asian converters, major suppliers to global beverage packaging chains, face acute feedstock constraints.

African markets: exposure without alternatives

African beverage markets, which source significant packaging inputs through the Gulf corridor, face a particular version of this problem: high exposure with limited domestic alternatives. The disruption has sharpened long-standing conversations about regional manufacturing investment, but those conversations were already advancing slowly and no near-term capacity expansion changes the current cost reality. For African producers running on spot pricing across packaging and freight, the margin pressure is immediate.

Rerouting is not a bridge

The shift to Cape of Good Hope routing is widely expected to outlast the immediate crisis. With the Red Sea already largely closed to commercial traffic due to Houthi interdiction, a separate disruption that predates the Hormuz closure, Maersk, CMA CGM, and Hapag-Lloyd have restructured scheduling around African routing, adding three to four weeks to key trade lanes. Those changes are operationally embedded regardless of what diplomacy achieves.

Supply chain specialists estimate that even after a resolution, rebuilding normal flow would take weeks of port clearance, vessel repositioning, and mine-clearing before trade could resume at scale. The cost environment beverage producers are managing now is substantially the one they will carry through the rest of 2026.

The procurement window is closing

Companies that have used the past eight weeks to lock in alternative supply, restructure freight exposure, and build recycled-content procurement have created measurable distance from those still operating on spot pricing. Nearshoring of packaging production and regionalisation of procurement, decisions that were on long-term roadmaps, are moving into near-term capital planning. The companies doing that work now are better placed than those waiting for the strait to reopen.

Read More

- Goldberg Brings Football Fans Back to Bars With Rewards Campaign Across Nigeria

- Craft Brewery That Survived Nigeria’s Mass-Market Beer War Builds a Global Name

- RTDs and Hard Seltzers Are Reshaping Alcohol Consumption in Africa